Assumption Life Insurance Review: What You Need To Know

Assumption life insurance review (2025 update)

Assumption life insurance is a longstanding Canadian company (originally founded in Massachusetts!) that sells term life insurance and permanent life insurance policies.

This company is known for its more lenient residency requirements, with policies available to holders of work permits, open permits, caregivers, and people on post-graduation work permits. It also has a higher-than-average age limit for no medical policies (85 years old) and plenty of add-ons to customize your coverage.

Assumption life insurance: Our verdict ★★★☆☆ (3.1/5)

Assumption Life has a middling industry reputation but above-average customer ratings. While Assumption Life’s policies are not the cheapest on the market, the company does excel in flexibility and variety — including guaranteed issue products.

Assumption has won several awards for its culture, sustainability, and philanthropy in recent years. It also has an A+ rating from the Better Business Bureau and an A- financial strength rating from A.M. Best.

Overall, this company is a good option for non-residents and people who seek no-medical life insurance.

Assumption life insurance: Key features

Assumption stands out from the crowd mostly for its non-resident coverage, but here are three more beneficial features:

- Mobile app ClaimSecure (iOS and Android)

- Thousands of customers across Canada

- Mostly positive reviews

Assumption life insurance pros and cons

You may be happy with Assumption Life’s coverage options, but your premiums probably won’t be the cheapest on the market.

Pros

Cons

Assumption life insurance cost and value

The cost of life insurance in Canada depends on your lifestyle risk factors and the coverage you want. The average cost is between $15 and $70 per month, but a good value will give you the coverage you need at a price that fits your budget.

At Assumption Life, the average Canadian will pay slightly more for coverage than with other major companies, like Sun Life or PolicyMe.

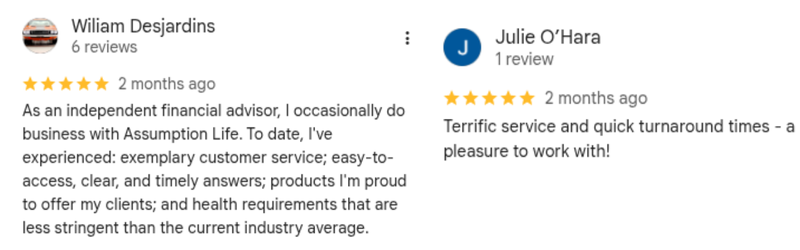

Assumption life insurance reviews and customer service

Assumption Life earns positive reviews for its customer service, with clients noting strong communication from advisors and quick response times. The company has a 4.1/5 star rating on Google and a 4.5/5 rating on Insureye.

Assumption life insurance products at a glance

Assumption Life offers term and permanent life insurance in four main types:

1. FlexTerm

- Customizable term life insurance with add-on riders

- Coverage between $50,000 and $10M

- Terms 10 to 35 years

- Individual or joint policy

- Ages 18 to 75 (ages 70 to 75 must go through full risk assessment)

- Automatic renewal up to age 90 with no medical exam required

- No medical exam may be required up to $999,999

- Built-in benefits include Extreme Disability Benefit and Insurability Benefit

2. Permanent life insurance

Assumption Life offers six types of permanent life insurance, from Essential Whole Life to Golden Protection.

- Essential Whole Life

- Bronze Protection (a guaranteed issue product with no payout in the first two years)

- Golden Protection (for ages 40 to 85 with coverage from $2,500 to $100,000)

- Several types of no medical exam insurance (varying questionnaires, age ranges, and coverage amounts)

3. Participating life insurance

With participating life insurance at Assumption, you may earn dividends by “participating” in investment strategies.

- Earn returns through a “participating” account

- Dividends are not guaranteed and may vary

There are two types of participating life insurance at Assumption Life:

- ParPlus: Coverage ranging from $5,000 to $4M for ages 18 to 70 (20-year pay) and ages 18 to 75 (payable for life)

- ParPlus Junior: Coverage ranging from $5,000 to $4M for ages 15 days to 17 years with no medical exam (payable over 20 years)

4. Living benefit: Critical protection insurance

- Ages 18 to 60

- Terms of 10, 20, 25, or up to age 75

- Coverage ranging from $10,000 to $100,000

- Pays out if you become disabled or critically il

- Covers 16 critical illnesses (fewer than other companies)

- Premiums are fixed for the term length

- May be renewable

How Assumption compares to other insurers

Let’s compare Assumption Life to three other major life insurance providers in Canada.

Assumption life insurance vs. PolicyMe life insurance

Both are good companies, but PolicyMe has a slight edge over Assumption Life:

- Cost: PolicyMe typically has more affordable options, though it depends on the policy.

- Customer experience: Both companies get stellar ratings, but PolicyMe has a slight edge.

- Industry reputation: Assumption Life has strong ratings from AM Best, but PolicyMe gets better overall ratings industry-wide.

The bottom line: Who should consider Assumption?

You may want to consider Assumption Life life insurance if you’re a non-resident in Canada, such as a worker, a caregiver, or a student. It’s also a good company for no-medical life insurance with general age limitations. Assumption doesn’t have the cheapest rates, but its customers report generally positive experiences with the company.

If you want similar flexibility and lower premiums, try PolicyMe, which offers affordable term life insurance policies and a streamlined digital experience.

FAQ: Assumption life insurance

.png)

Our mission is to empower Canadians to make informed financial decisions. To achieve this, we have an expert editorial team that includes licensed insurance advisors and financial planners. We prioritize the best interests of Canadian families and won't endorse any product, company or financial strategy that we believe isn't suitable. Our educational guides are crafted by in-house experts, like licensed life insurance advisors. Before publication, we subject our research and advice to scrutiny and comprehensive revisions for accuracy and completeness.

Our mission is to empower Canadians to make informed financial decisions. To achieve this, we have an expert editorial team that includes licensed insurance advisors and financial planners. We prioritize the best interests of Canadian families and won't endorse any product, company or financial strategy that we believe isn't suitable. Our educational guides are crafted by in-house experts, like licensed life insurance advisors. Before publication, we subject our research and advice to scrutiny and comprehensive revisions for accuracy and completeness.